These monthly market commentaries share a synopsis of the U.S. financial markets with intelligent insights.

March 2026 Market Recap

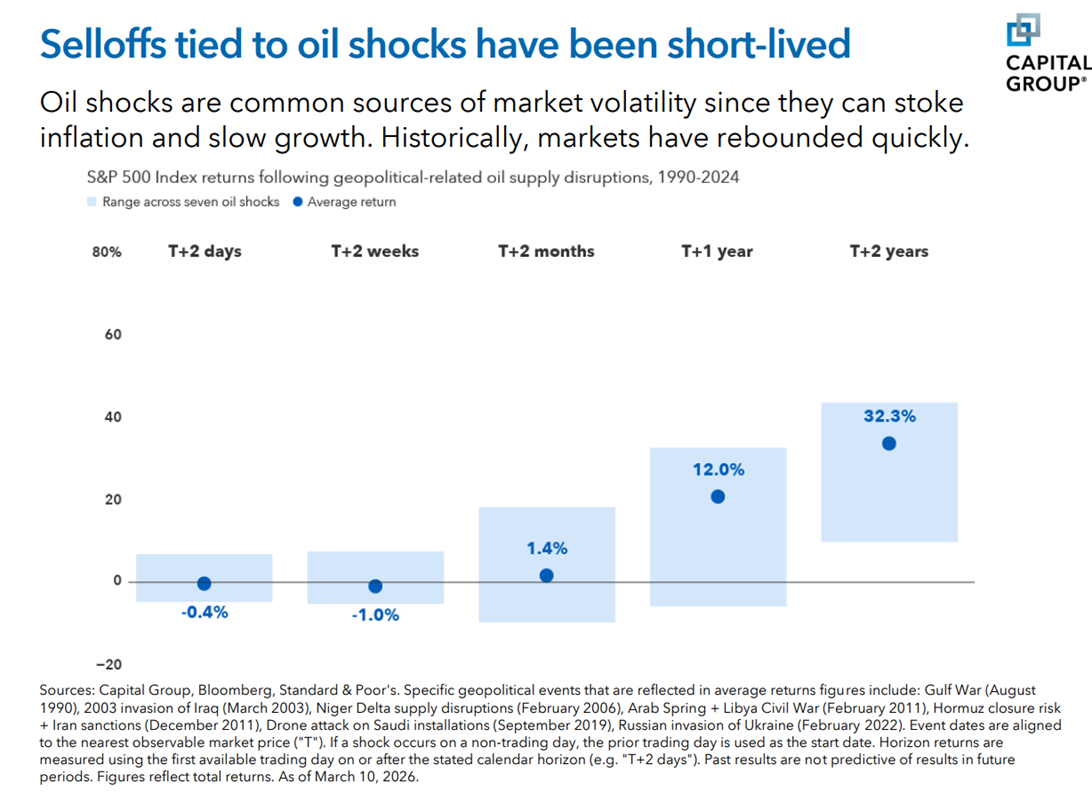

After the initial uncertainty following oil supply disruptions, equity markets have often recovered quickly. Over the past two decades, energy markets have generally bounced back from geopolitical shocks, since these events haven't led to prolonged physical supply outages.

Thus, big moves in commodities and equity prices rarely last. Part of the reason is that the United States, the world's leading consumer of oil and gas, is now also its largest producer. No two events are the same, and the war with Iran feels especially close to home given direct U.S. involvement. As globalization continues to evolve, markets may increasingly face sudden disruptions.

Here are observations on what occurred across the investment markets in March:

Broad Market Performance1

| Index | March | Q1 | 1 Year | 3 Year |

| S&P 500 | -5.0 | -4.3 | 17.8 | 18.3 |

| MSCI EAFE | -10.3 | -1.2 | 21.3 | 13.6 |

| Bloomberg US Aggregate Bond | -1.8 | -0.1 | 4.4 | 3.6 |

Data as of March 31, 2026

Domestic Equity2

International and Global Equities3

Fixed Income Markets4

Specialty Markets5

Sectors6

Market Volatility

Oil shocks are common sources of market volatility, as they can stoke inflation and slow growth. Historically, markets have rebounded quickly. See chart below:

Dear Valued Investor,

As the Iran conflict enters its second month, geopolitical stress continues to test investors. Historical stock market performance during geopolitical conflicts helps remind us that stocks are far more resilient than the moment may suggest. As we assess today’s environment and the uncertainties surrounding ongoing military operations in Iran, we focus on two past conflicts we believe are instructive, though past performance does not guarantee future results.

The two periods offer contrasts. In 1990, at the start of the first Gulf War, the U.S. economy was slipping into recession. Corporate profits were flattening, inflation remained elevated, and consumer confidence was fragile. With little fundamental support in place, markets initially struggled. Yet even then, equities began recovering well before the conflict formally ended, anticipating eventual stabilization.

By contrast, in 2003, when the Iraq War began, the economy had already healed from the dotcom bust and the 2001–2002 corporate accounting scandals. Corporate earnings were rebounding, monetary policy was supportive, and valuations were reasonable. With stronger fundamentals in place, markets responded positively after hostilities started and began a five-year bull market that didn’t peak until October 2007.

Today, we see elements of both periods, but importantly, we do not see evidence that the long‑term economic or earnings outlook has been meaningfully impaired. First and foremost, a demilitarized Iranian regime would ultimately contribute to a safer world and more stable markets, mitigating a key geopolitical risk that has persisted for nearly five decades. From a market perspective, nothing about the current conflict undermines our confidence in the long‑term attractiveness of equities. For stocks, the more positive 2003 path seems more likely than 1990.

Beyond the human element, we can all acknowledge that this environment is uncomfortable. The damage the Iranian regime has inflicted on energy and other infrastructure in the region is unsettling. Iran maintains control of the Strait of Hormuz. There is no easy off-ramp. Yet history shows that markets often recover well before geopolitical tensions are fully resolved, frequently with surprising force once clarity begins to emerge. As stocks hinted at with strong gains on the last day of March, that outcome remains possible in our view.

While no one can predict how long this period of volatility will last, the underlying economic foundation and corporate America’s earnings power remain strong. Attractive opportunities are likely to emerge from this downdraft once U.S. military objectives are achieved and tankers can move freely through the strait.

We believe it's important to keep portfolio risk at or near long-term targets and remain well diversified. For long-term focused investors, we see opportunities to take advantage of weakness.

Warmest regards,

Helpful Resources:

View our Economic Market Minutes: https://www.gocgo.com/market-minute

Financial Planning Webinars: https://www.gocgo.com/financial-resource-library

Firm Website: https://www.gocgo.com/financial-planning-and-wealth-management

Investor Blog: https://www.commonfinancialsense.com/

Disclosures and references:

Investment Advisory Services offered through Global Retirement Partners, LLC DBA Connor & Gallagher OneSource, an SEC registered investment advisor.

1-6 All data referenced in the table and comments supplied by Morningstar.

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from Global Retirement Partners, LLC or any of its subsidiaries to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision, and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professionals, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for informational purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not reliable indicators of current and future results.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. Connor & Gallagher OneSource doesn’t provide research on individual equities. All information is believed to be from reliable sources; however Connor & Gallagher OneSource makes no representation as to its completeness or accuracy.

*Securities offered through LPL Financial, Member FINRA & SIPC. Investment advisory services offered through Global Retirement Partners, LLC DBA Connor & Gallagher OneSource, an SEC registered investment advisor. Connor & Gallagher OneSource and Connor & Gallagher Benefit Services are separate entities from LPL Financial.