These monthly market commentaries share a synopsis of the U.S. financial markets with intelligent insights.

Latest Commentary:

May 2026 Market Recap

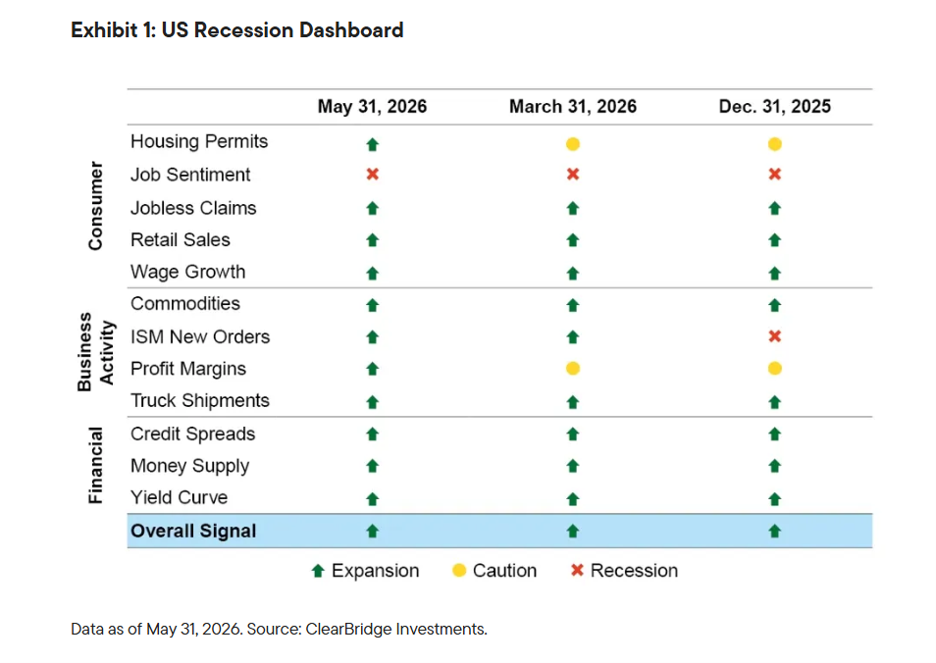

Are we headed for a recession? No.

Here’s our monthly AOR Anatomy of a Recession US dashboard from Clearbridge Investments that we review weekly.

The strong rally in April continued into May as investors rode the AI growth theme and focused on strong Q1 earnings across most sectors. In the U.S., the S&P 500 was up 5%, the Russell 2000 was up more than 4% and the tech-heavy NASDAQ 100 rose more than 10%. Growth outperformed value and large outperformed small as the market narrowed further. Non-U.S. stocks lagged the U.S. though they sustained their April momentum. MSCI EAFE returned 3% while MSCI Emerging Markets rose 10%, driven by South Korea’s 30% rally in May. The bond market was largely flat for the month, with the Bloomberg Agg index returning 0.3%. U.S. interest rates rose during the middle of the month and held steady into the month end. Investors focused on higher inflation levels and lowered their expectations for rate cuts.

Here are observations on what occurred across the investment markets in May:

Broad Market Performance1

| Index | May | YTD | 1 Year | 3 Year |

| S&P 500 | 5.3 | 11.3 | 29.8 | 23.6 |

| MSCI EAFE | 3.1 | 9.4 | 22.8 | 18.2 |

| Bloomberg US Aggregate Bond | 0.3 | 0.4 | 5.1 | 4.0 |

Data as of May 31, 2026

Domestic Equity2

International and Global Equities3

Fixed Income Markets4

Specialty Markets5

Sectors6

Key Points:

Job Market Update as of 6/6/2026

US Unemployment Rate remained at 4.3% in May, the lowest level since last August & well below the historical average of 5.7%. 172k jobs were added vs. 85k expected. March/April jobs were revised up 93k. YoY wage growth: +3.4%. Overall: strong report, no Fed rate cut this month.

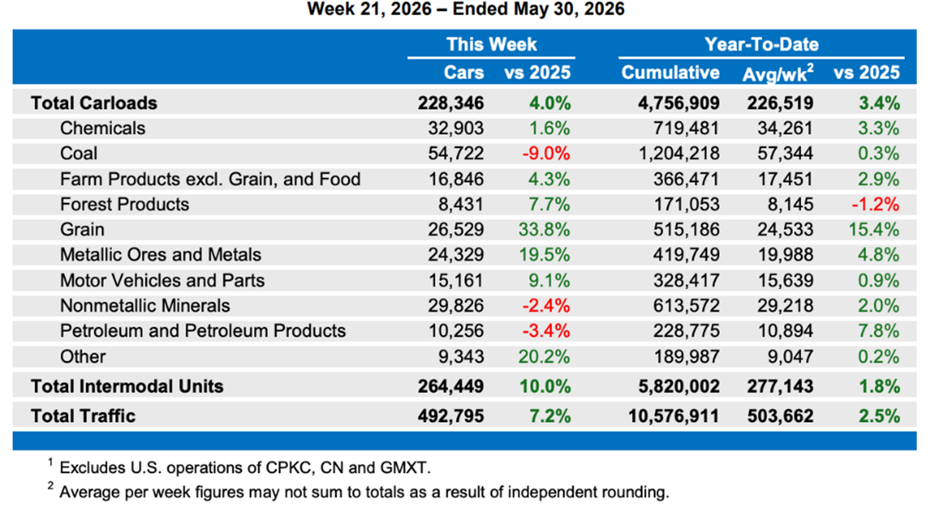

One Main Reason We Are NOT Heading Into a Recession...

Quietly, the industrial economy has been resurging…according to the Association of American Railroads carloads were up 7.2% last week of May versus last year…and pretty much every category is up year over year thus far in 2026…

We all need to be aware of inflation, it's the silent killer for our budgets now and in the future, especially since most of us live on a budget. Budgets are necessary saving for retirement and especially living in retirement. Our investments need to have growth to beat inflation.

Inflation facts to be aware of:

By The Way...

Here's My Stock Market Outlook: 3 Themes for the Second Half of 2026

Dear Valued Investor,

Equity markets have continued their advance in recent weeks, with the S&P 500 near a record high following a rare nine-week winning streak on strong AI-driven earnings and prospects for an Iran agreement. While the macro backdrop remains mostly constructive, valuations are elevated by most traditional metrics, and oil remains near $100 with the Strait of Hormuz still closed. Is the stock market pricing in too much good news?

To answer this question, we suggest not putting much emphasis on valuation. Valuation metrics such as the price-to-earnings ratio (P/E) are helpful in assessing long-term return potential and downside risk, but they are historically poor market timing tools. The S&P 500’s P/E near 21 can be justified by solid earnings growth and a resilient U.S. economy, although further expansion will require continued cooperation from key drivers such as inflation (oil prices) and interest rates. Unless these macro inputs improve, returns in the second half of the year are likely to be modest, potentially with some bumps along the way.

Against this backdrop, the role of AI remains central. Technology companies, particularly the mega cap hyperscalers, have continued to deliver compelling earnings growth, even as skepticism around the magnitude of investment and timing of eventual returns persists. Results have continued to point to accelerating investment and demand for computing resources. Some big moves in semiconductor and IT hardware companies over the past week suggest the market has not quite caught up to the magnitude of these investments – expected to exceed $750 billion this year and up about 50% since 2026 began.

While valuations appear elevated at the index level and speculation in certain market segments may have gone too far, parts of the technology sector may actually be undervalued relative to their growth potential. Skepticism about the productivity gains AI will bring remains widespread, leaving room for potential upside surprises. At the same time, heavy AI-related capital expenditures have depressed free cash flow, which introduces risk if anticipated productivity gains fail to materialize.

Looking ahead, the market narrative will continue to hinge on the intersection of valuations and AI-driven earnings growth. Elevated multiples and sticky inflation suggest more limited upside from higher valuations, placing greater importance on earnings to come through. AI remains a powerful tailwind for both economic activity and corporate profits, supporting the case for staying invested. The promise of what AI can bring is exciting, but the optimism may be getting ahead of what the technology can deliver. As a result, maintaining discipline around diversification and risk management takes on greater importance.

If you have any questions, please feel free to reach out at your convenience.

Thank you for your trust along your financial journey.

Helpful Resources:

View our Economic Market Minutes: https://www.gocgo.com/market-minute

Financial Planning Webinars: https://www.gocgo.com/financial-resource-library

Firm Website: https://www.gocgo.com/financial-planning-and-wealth-management

Investor Blog: https://www.commonfinancialsense.com/

Previous Commentary:

Disclosures and references:

Investment Advisory Services offered through Global Retirement Partners, LLC DBA Connor & Gallagher OneSource, an SEC registered investment advisor.

1-6 All data referenced in the table and comments supplied by Morningstar.

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from Global Retirement Partners, LLC or any of its subsidiaries to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision, and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professionals, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for informational purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not reliable indicators of current and future results.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. Connor & Gallagher OneSource doesn’t provide research on individual equities. All information is believed to be from reliable sources; however Connor & Gallagher OneSource makes no representation as to its completeness or accuracy.

*Securities offered through LPL Financial, Member FINRA & SIPC. Investment advisory services offered through Global Retirement Partners, LLC DBA Connor & Gallagher OneSource, an SEC registered investment advisor. Connor & Gallagher OneSource and Connor & Gallagher Benefit Services are separate entities from LPL Financial.